Japan’s Bid to Bring Money Home Faces Fiscal, BOJ Reality Check

The Japanese government’s push for pension funds and individuals to invest more in domestic markets is seen as a potential boost for the nation’s bonds and currency in the long term, but less likely to have significant near-term impact without changes to fiscal and monetary policy.

Analysts broadly agree that redirecting more domestic savings into Japanese assets could provide a long-term source of demand for government bonds and support the yen. But they say investors remain more focused on Prime Minister Sanae Takaichi ’s expansionary fiscal agenda, expectations for only gradual Bank of Japan policy tightening and still-wide interest-rate differentials.

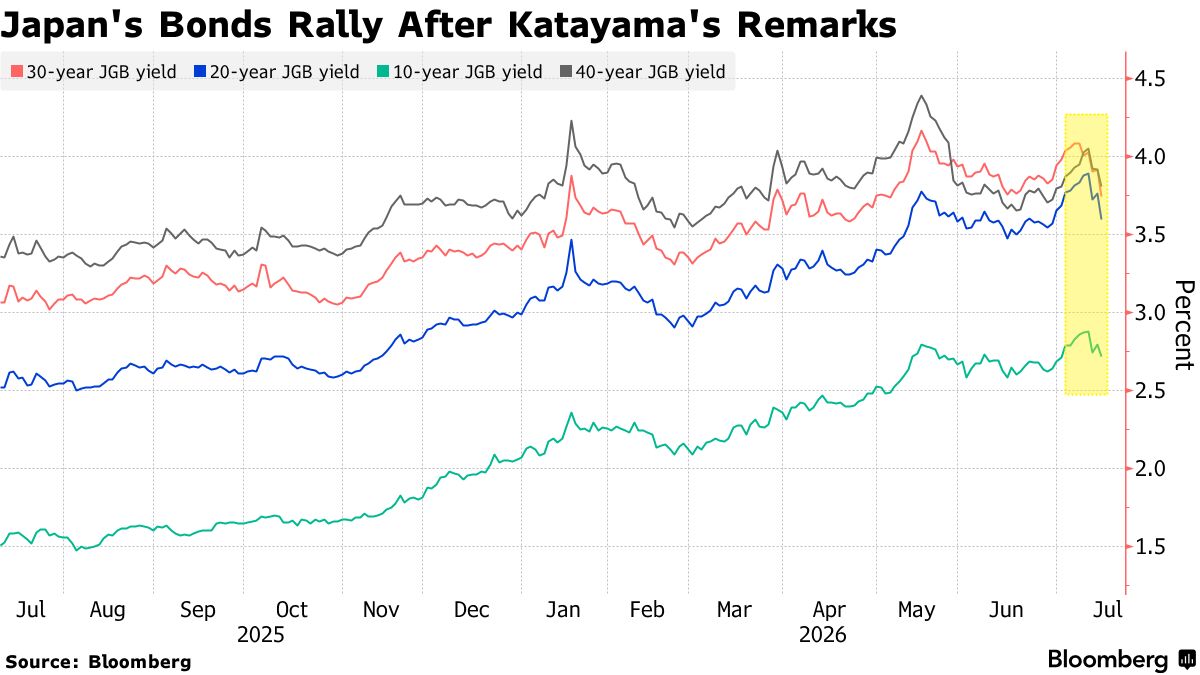

Finance Minister Satsuki Katayama recently urged Japan’s large pension funds, including the Government Pension Investment Fund, to increase investment in domestic assets and floated the idea of adding government bonds to a tax-free investment program for individuals. The remarks sparked a rally in sovereign bonds and, to a lesser extent, the yen, as investors speculated that encouraging more money to stay at home could help reverse years of capital outflows.

The potential flows are sizeable. Societe Generale SA the GPIF alone could buy about $76 billion of additional Japanese government bonds by raising domestic bond holdings to the upper end of its existing allocation range without changing its strategic asset allocation. Deutsche Bank AG estimates broader repatriation by pension funds, insurers and retail investors could eventually total as much as $440 billion.

Yet many investors question how quickly those flows can materialize. Laura Cooper , global investment strategist and head of macro credit at Nuveen, cautioned against chasing the rally in Japanese government bonds.

“While it shows the market is eager to add duration and Katayama finally flagging this as an option could drive repatriation flows in FY2027, there needs to be greater clarity on the fiscal and rate-hiking paths,” she said. Reduced BOJ bond purchases, elevated government debt issuance and the rebuilding of term premia continue to dominate the outlook, Cooper added.

Read more:

The renewed focus on domestic investment comes as Tokyo seeks new ways to support Japanese assets after repeated foreign-exchange interventions failed to halt the yen’s slide. Despite spending a record ¥11.73 trillion ($73.4 billion) buying the currency earlier this year, the yen remains near its weakest level against the dollar in four decades.

At the same time, the BOJ is steadily reducing its bond purchases, increasing the need for private investors to absorb growing government debt issuance. That has sharpened interest in whether pension funds, insurers and households could gradually redirect some of the trillions of dollars invested overseas over recent decades back into domestic markets.

Still, pension fund purchases of super-long Japanese government bonds may not increase as much as the market initially anticipated, Morgan Stanley MUFG Securities strategists including Koichi Sugisaki wrote in a note.

The government’s initiative is likely to focus more broadly on encouraging domestic investment across the financial system, rather than directing demand specifically toward government bonds, they said. “From a domestic bond perspective, therefore, the announcement may be mainly a verbal intervention that keeps repatriation risk ‘alive.’”

Markets remain concerned that Takaichi’s ambitious spending plans will increase government debt issuance, while the BOJ is expected to normalize monetary policy only gradually despite persistent inflation. Overnight index swaps imply traders expect just one additional quarter-point rate increase this year, leaving Japan’s interest-rate disadvantage largely intact.

“It does appear that the Ministry of Finance is exploring ways of supporting the yen beyond intervention,” said Jane Foley , head of FX strategy at Rabobank. “But the government will still need to provide greater reassurance on fiscal policy, while the Bank of Japan will have to demonstrate it is not falling behind inflation before Japanese government bonds become sufficiently attractive to accelerate repatriation.”

For Vishnu Varathan , head of macro research for Asia ex-Japan at Mizuho Bank, the proposal for the GPIF to increase investment in domestic assets may be enough to deter the most aggressive speculative bets against the yen, but not enough to reverse the broader trend.

“Even this may only deter the most speculative end of the bearish spectrum,” he said. “In other words, merely stalling yen bears, not seducing self-sustaining bulls.”