PBOC’s New Overnight Rate Said Below Forecasts in Hint at Easing

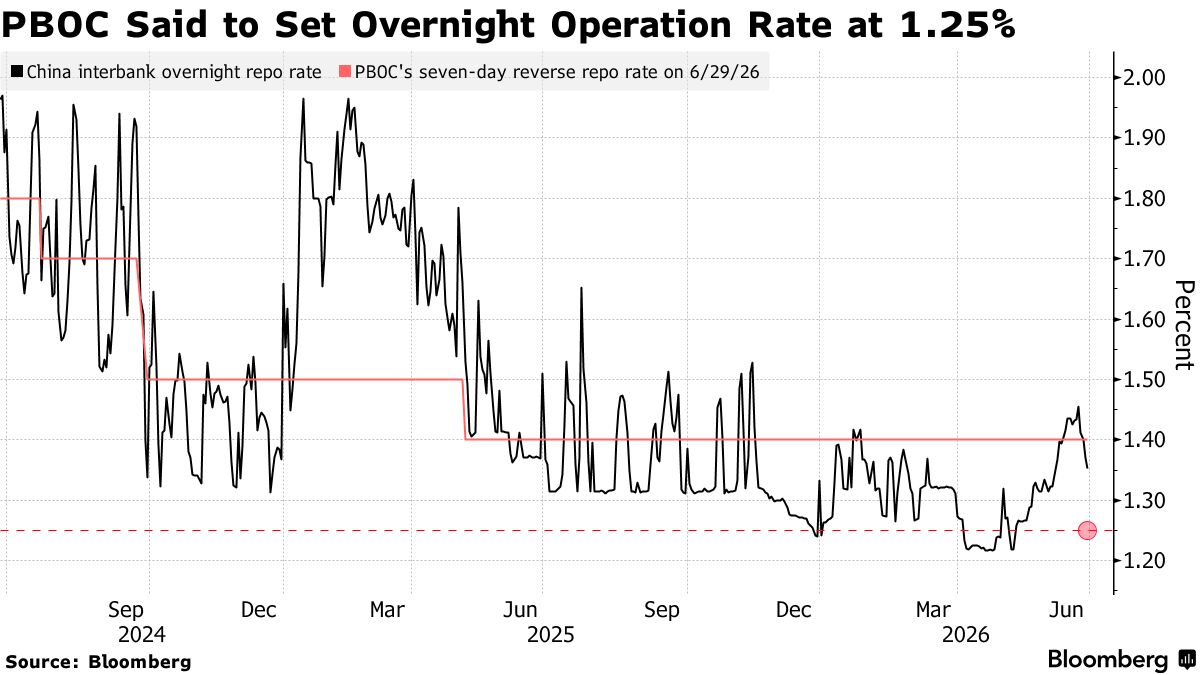

China’s central bank set the interest rate on its new overnight liquidity tool at a level that was below expectations, according to people familiar with the matter, in what some economists see as a de facto rate cut that could push down market borrowing costs.

The People’s Bank of China said it conducted 300 billion yuan ($44 billion) of overnight reverse repurchase agreements in open market operations on Monday, according to a statement that didn’t disclose the rate of interest it charged on its new instrument. The central bank uses the operation to funnel short-term funds to the market to influence borrowing costs, and it accepts eligible bonds as collateral.

The cost of the facility came in at 1.25%, the people said, asking not to be named because they weren’t authorized to speak publicly. That compares with the median forecast of in a Bloomberg survey of analysts and economists.

The PBOC ’s benchmark remained at 1.4%, as it provided 157.5 billion yuan of seven-day reverse repo. The central bank didn’t immediately reply to a Bloomberg fax seeking comment.

The decision sets the stage for looser monetary policy including a possible cut in loan prime rates — China’s lending benchmarks — as early as next month, according to Citigroup Inc. and Standard Chartered Plc.

“Today’s move is not an outright easing, in our view — but it likely opens the door to one,” Citigroup economists led by Xiangrong Yu said in a note. “The asymmetric move likely signals an easing bias, without a formal cut.”

The operation marks the first time that the PBOC is deploying the tool to manage liquidity, and some traders said the move could be a first step in a gradual shift toward a benchmark overnight rate. Such a transition is likely to bring China closer to the practice of its global peers such as the Federal Reserve, which relies heavily on its overnight target rate to manage the US economy.

The new facility is expected to give the PBOC better control over short-end borrowing costs and allow it to smooth out any big swings in market liquidity. The cost of overnight borrowing in the interbank market has become more volatile since May, as the central bank sought to ease a glut of money in the financial system, with demand for cash typically rising at the end of each quarter.

The yield on China’s 10-year government bonds slipped one basis point to 1.71% after the announcement, extending its drop into a third session. Both the overnight and seven-day repo rates eased.

But some analysts said the PBOC may be looking to maintain the policy status quo, for now, by keeping the seven-day benchmark steady while publicly omitting details about the new overnight rate.

“The overnight reverse repo is primarily a liquidity tool aimed at smoothing seasonal funding stress, rather than a tool to signal a particular policy stance,” said Frances Cheung , head of foreign exchange and rates strategy at Oversea-Chinese Banking Corp. “The timing of the operations today and tomorrow ahead of the half-year end — and the amount bigger than the seven-day reverse repo — both support this notion.”

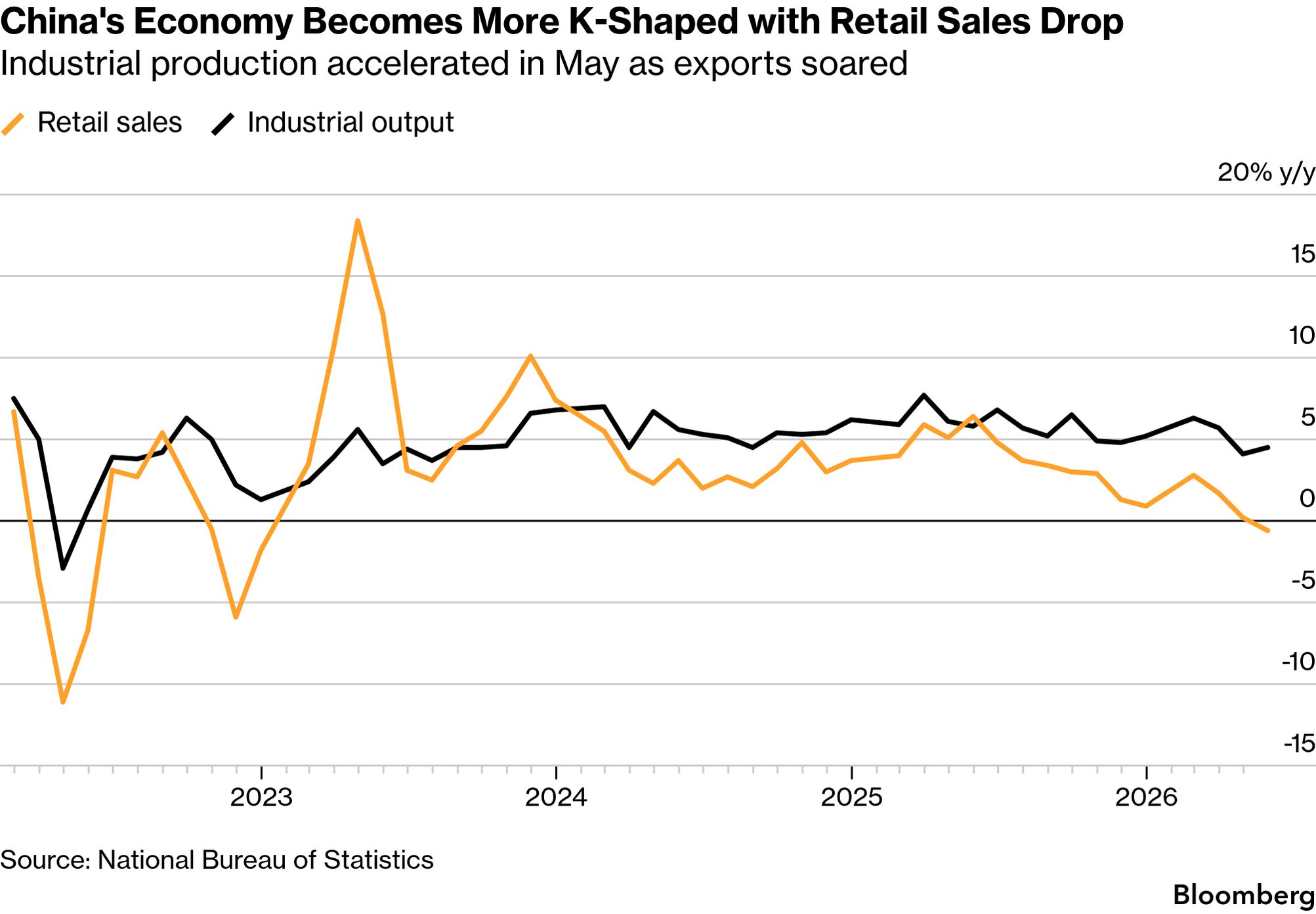

Talk of a rate reduction has gained some traction as the Chinese economy slowed sharply in the second quarter, with retail sales and investment falling at a pace unseen since the pandemic. Most economists expect the PBOC to keep its policy rate unchanged throughout 2026, although Huang Yiping , an adviser to the central bank, said a still remains a possibility.

CHINA REACT: Low Overnight Rate Shows PBOC Ready to Ease Further

“The next step is to lower de facto lending rates, including a possible reduction of LPR rates” — across both one- and five-year durations — “to support a stabilization of credit growth,” said Becky Liu , head of Greater China macro strategy at Standard Chartered.

“We had long argued that China is firmly staying on an easing path, and will likely to take advantage of the interest rate framework reform to lower de facto rates,” she said.

Lynn Song , chief Greater China economist at ING Bank NV, said it’s possible the new rate may have been kept undisclosed to avoid “diluting” the significance of the seven-day benchmark.

“Given the overnight rate is still the most liquid and important rate for trading activity, it makes sense this will eventually be the level that policymakers seek to control,” Song said. “However, it probably will take some time. We probably need some track record and maturity for the overnight repo facility and how it affects market overnight rates before this shift is made.”