South Korea Opens 24-Hour Won Trading at a Fraught Moment

Deep inside a government complex in Sejong, about two hours from Seoul, a room known as “the box” is ground zero for South Korea’s currency anxieties.

Behind a door marked “restricted access,” finance ministry officials watch every tick in the won, scrutinizing price swings and trading volumes to determine when intervention might be necessary. Tensions are high as the currency dropped to a 17-year low and was the worst performer in Asia in the first half.

From July 6, their task will be even more challenging as the won will trade around the clock for the first time. Preparations have ramped up: meals are upgraded, an extra official has joined, and a rickety camping cot may soon be replaced with a proper bed, according to a person with knowledge of the matter, who asked not to be identified discussing private information.

To the developed world, which takes 24-hour currency trading for granted, it might not seem such a big deal. But the shift is an unprecedented loosening of South Korea’s grip on its currency, a policy shaped by the trauma of the 1997 Asian financial crisis that nearly brought the economy to its knees.

The change is central to Seoul’s bid for an MSCI Inc. upgrade to , which would cement its place as a global investment destination. It also reflects how the economy evolved from a manufacturing juggernaut focused on bringing export earnings home to one investing more overseas, making it harder to justify limiting won trading to Korean business hours.

“The extended trading hour is a necessary move to increase its presence in the global financial markets,” said Claire Huang , senior Asia macro strategist at Amundi Asset Management. “Facilitating won transactions at a level comparable to G10 currencies requires securing liquidity during extended hours.”

But Korea’s big move comes at a delicate time.

Launching onto the global stage just as the won is revisiting levels last seen in 2009 leaves the currency and economy more open to speculators. A misstep by regulators may amplify volatility, embolden bearish bets and undermine the investment narrative that has put the country at the center of the global artificial-intelligence boom.

As the won slid past 1,400 per dollar, a level President Lee Jae Myung once said signaled broad economic strain and pressure on households, officials repeatedly against speculative trading. This year, regulators major banks for activity deemed destabilizing to the market, and exporters were urged to convert their export proceeds to help stabilize the local currency.

Even so, the won has kept falling, last trading at around 1,550 per dollar, leaving it down more than 7% this year.

The currency’s weakness is at odds with a booming economy and surging equities. The benchmark Kospi Index has jumped about 80% this year, the strongest run of any major global equity gauge, powered by an AI frenzy that has turned and into trillion-dollar giants. Exports are hitting record highs and the current-account surplus — at about $28 billion in April — is among the largest Korea has ever posted.

To understand the disconnect, it helps to look at how things used to work: for decades, strong exports and persistent current-account surpluses supported the won. Exporters repatriated earnings and foreign investors poured money into Korean assets.

That dynamic is faltering. South Korea posted a $102.7 billion current-account surplus in the first four months of the year. But much of that inflow is offset by capital outflows – over $60 billion from outbound direct investment and local investors buying foreign securities – while global investors have some $43.6 billion from Korean equities.

In effect, Korea is increasingly behaving like a capital exporter. It continues to earn dollars from trade, but that money is being invested overseas rather than recycled into local markets.

“This transparency proves Korea is committed to international standards,” said Ali Bora Yigitbasioglu , senior investment manager of emerging-market fixed income at Pictet Asset Management. “While directional exposure still depends on the semiconductor export cycle, removing these operational friction points makes holding Korean assets structurally more attractive.”

Other factors are adding pressure on the currency. The National Pension Service has been increasing its overseas investments, a shift that involves buying dollars and selling won, although it pared back those plans this year. Investors are also worried about the , under which Seoul has promised to invest $350 billion in America.

Still, Seoul is to the change. “This isn’t merely a regulatory reform — it is a critical piece of infrastructure that enables Korea’s capital markets to achieve the level of accessibility and convenience expected of developed markets,” Moon Jisung , Korea’s deputy finance minister, said in an interview.

Arbitrage Trades

The global FX market runs around the clock during the week, allowing counterparties to hedge risks as markets move. That has been the norm since major currencies began floating freely in the early 1970s, evolving into a market that now turns around across Asia, Europe and North America.

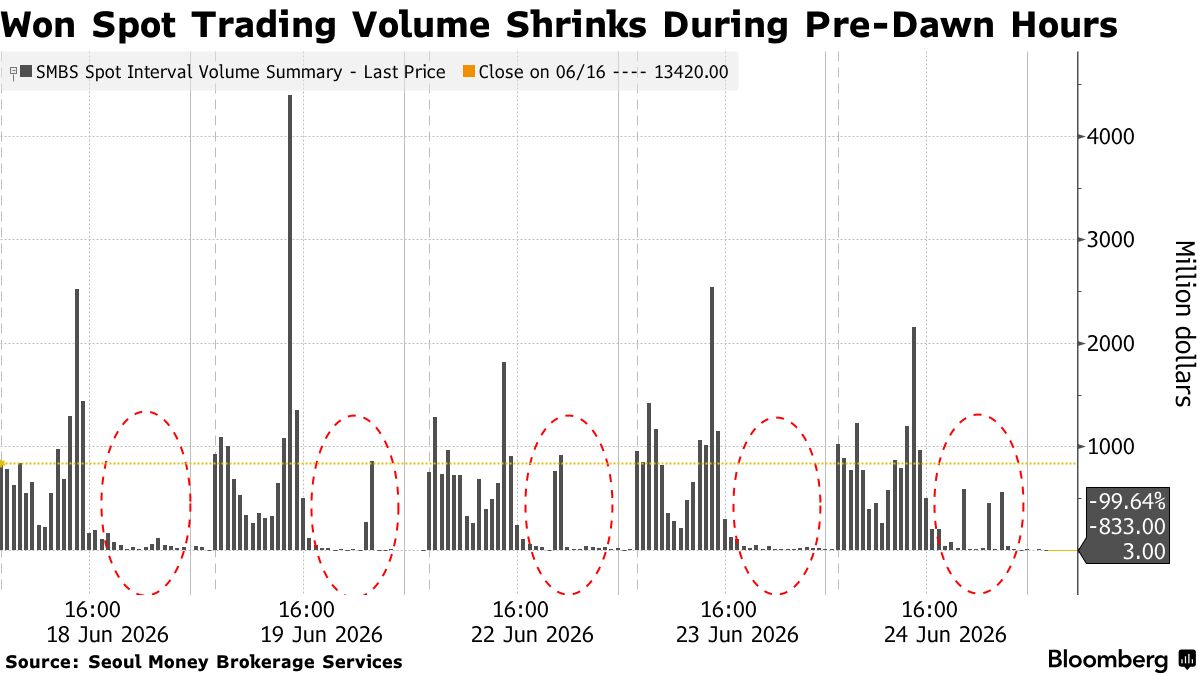

Currently, the won trades for 17 hours before the market shuts from 2 a.m. to 9 a.m. in Seoul, a window that overlaps with the US trading day.

The break has frustrated global investors. Anyone buying Korean stocks takes on exposure to the won, but once the onshore currency market closes, investors have little choice but to manage that risk offshore through non-deliverable forwards, or NDFs, contracts that settle without actually exchanging the currency.

Heavy use of NDFs creates a class of arbitrage traders who exploit price gaps between offshore and onshore markets, adding the kind of volatility that regulators frown upon.

The shift to 24 hours — from Monday morning to Saturday morning — will eliminate that gap. Authorities are also introducing hourly benchmark pricing, easing foreign-investor reporting rules and allowing offshore spot won trading from next year.

In theory, continuous trading should smooth price action, though benefits may take time to emerge. “Greater market openness is likely to come with higher volatility, and that is something policymakers should keep in mind,” according to Bumki Son , an economist at Barclays Plc.

Banks are racing to prepare. Woori Bank , one of the country’s largest lenders, secured a UK license late May to support won-related transactions and investments outside Korean market hours. Most major banks have , or are expanding, their dealing teams in London and Seoul.

Investors see new trading prospects too. “There will be a lot of people trying to access the market as a carry trade opportunity,” said Ed Al‑Hussainy , a portfolio manager at Columbia Threadneedle in New York, referring to a strategy where investors borrow a low-yielding currency to invest in assets with higher returns.

Building Buffers

South Korea has been preparing for this moment for years.

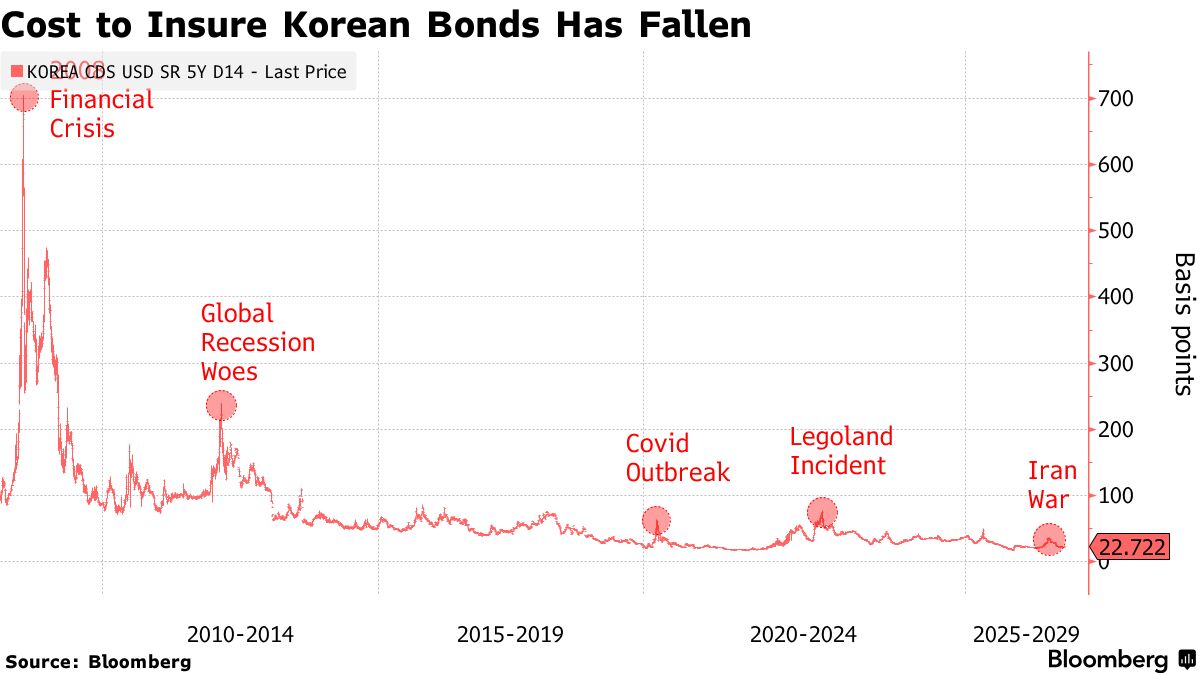

Many of today’s senior government officials were on the front lines of the 1997 Asian financial crisis when the won lost half of its value within the span of two months. Then Korea was teetering on the brink of default, as short-term foreign debt ballooned and conglomerates were collapsing.

“The won was plunging more than 10% a day, with swings at times exceeding 20%,” recalled Lew Changbeom , a former currency trader at Bank of America NA and JPMorgan Chase & Co. “I truly feared the country might collapse.”

The takeaway was clear: never again be caught short of dollars. Korea rebuilt its foreign reserves – once down to just four to five days of import cover – and tightened its grip on the currency, restricting trading hours, keeping settlement onshore and channeling transactions through designated banks.

Today, it sits on one of the largest foreign reserve stockpiles in the world, giving it a war chest to support its currency against global pressures.

Back inside the box, officials are just one call away from key decision makers in Seoul or banks to act quickly if the market suddenly turns. But with 24-hour trading on the horizon, the efficacy of such tactics may diminish.

“Foreign exchange authorities should move away from the idea that the market needs to be tightly controlled,” said Seungheon Lee , the former senior deputy governor at the Bank of Korea. “To achieve tangible results, we must resolve the mechanisms that prevent trading from taking place.”