India FX Buffer Is Still Robust to Defend Rupee, Economists Say

India’s foreign-exchange reserves remain strong enough to defend its currency against the Iran-war driven oil shock, with buffers well above stress levels seen during the taper tantrum, according to economists.

The Reserve Bank of India can deploy nearly $150 billion from its forex pile of $690 billion before import cover falls to 2013 levels, when the Federal Reserve’s plan to scale back bond purchases triggered outflows from emerging markets, calculations based on economists’ estimates show.

The central bank’s reserves, despite being among the world’s biggest, are facing tougher scrutiny from investors as the rupee hits record lows. The country will likely fall short of foreign flows for an unprecedented third year to meet a wider current account gap as crude prices stay elevated.

While a prolonged crisis in the Middle East will reduce the comfort on FX reserves, “the situation isn’t as dire as the taper tantrum,” said Gaura Sen Gupta , chief economist at IDFC First Bank Ltd. India is better off than in 2013 on several counts, including capital flows and short-term debt as a percentage of reserves, she said.

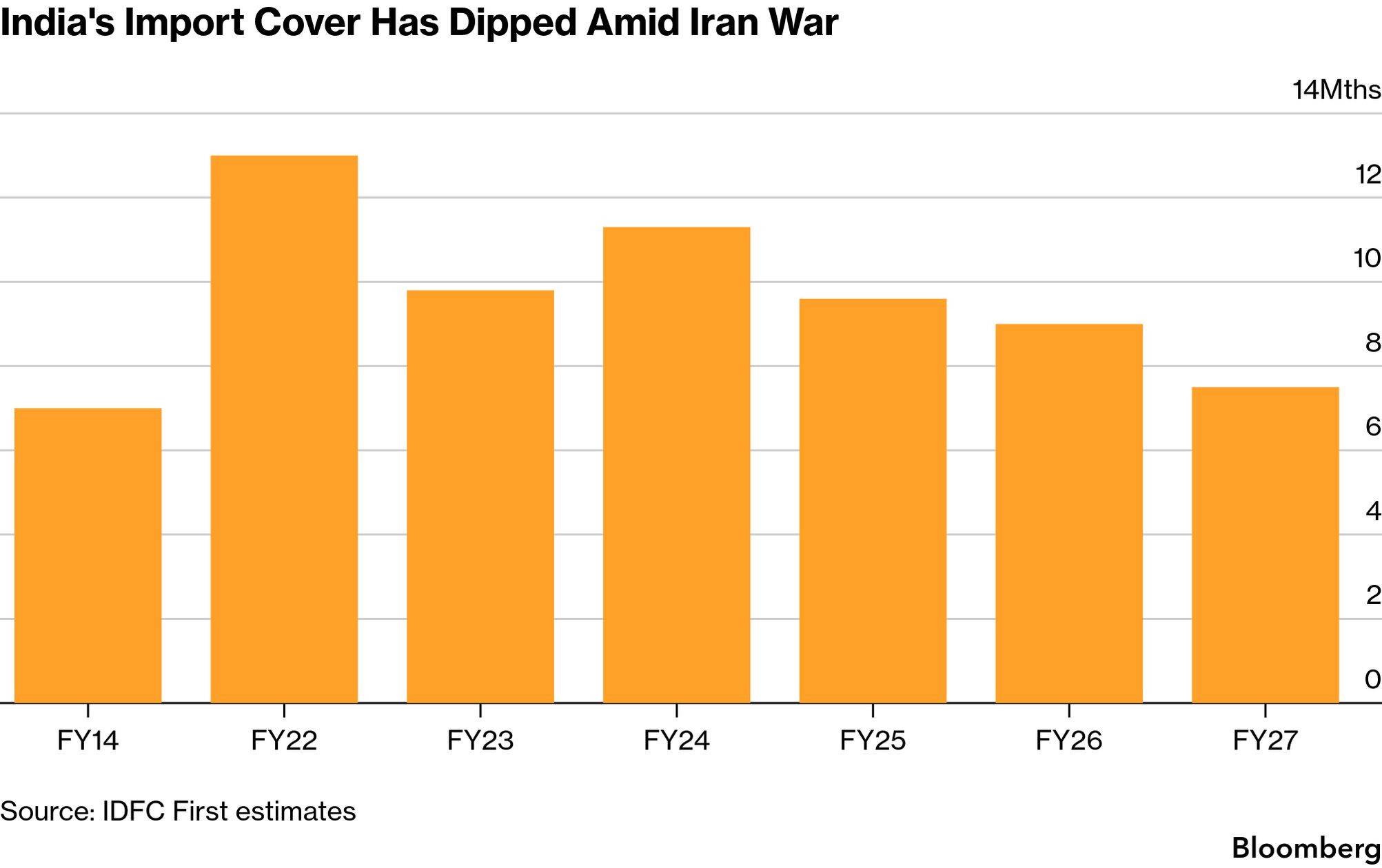

During the taper tantrum, India’s import cover, a key metric that measures the number of months a country can pay for its inbound shipments using reserves, dipped to less than seven months. It currently stands at about nine months after factoring in the central bank’s future dollar obligations, and is expected to fall below eight months by March 2027, according to IDFC First Bank.

An by Prime Minister Narendra Modi over the weekend to conserve foreign reserves has put the spotlight on the nation’s external finances. The government this week import duties on gold and silver, and markets are speculating more steps may be in the offing to boost inflows or even curb outflows.

India’s forex cover has dropped by $38 billion since the Iran war started, the most in the region. Complicating matters, the RBI faces about $103 billion in derivative-related obligations from past efforts to support the rupee, Asia’s worst-performing currency this year with a 6% decline against the dollar.

“This time around, the desired threshold for any metric to assess FX reserves adequacy will be higher versus previous episodes, even at the same level of crude oil prices, given weak capital inflows,” said Anubhuti Sahay , head of India economic research at Standard Chartered Plc in Mumbai.

Still, India is facing global uncertainty from a much stronger footing with both fiscal and external deficits in check and benign inflation.

Read More:

“Most FX reserves adequacy metrics indicate a comfortable position for India,” said Madhavi Arora , chief economist at Emkay Global Financial Services. “We are far from the taper tantrum period of 2013, with policymakers having worked on keeping the internal and external balance sheets of the economy well in check.”