Why Korean Pension Fund’s New Hedging Policy Supports Won

South Korea’s largest pension fund removed its cap on currency hedging last month, allowing it to exercise more heft in the foreign exchange market at a time of won weakness.

The National Pension Service , which manages about ($1.08 trillion), in April that a 15% ceiling on forex hedging for its foreign investments is now a baseline. The change lets it smooth out volatility in the currency market caused by its capital outflow.

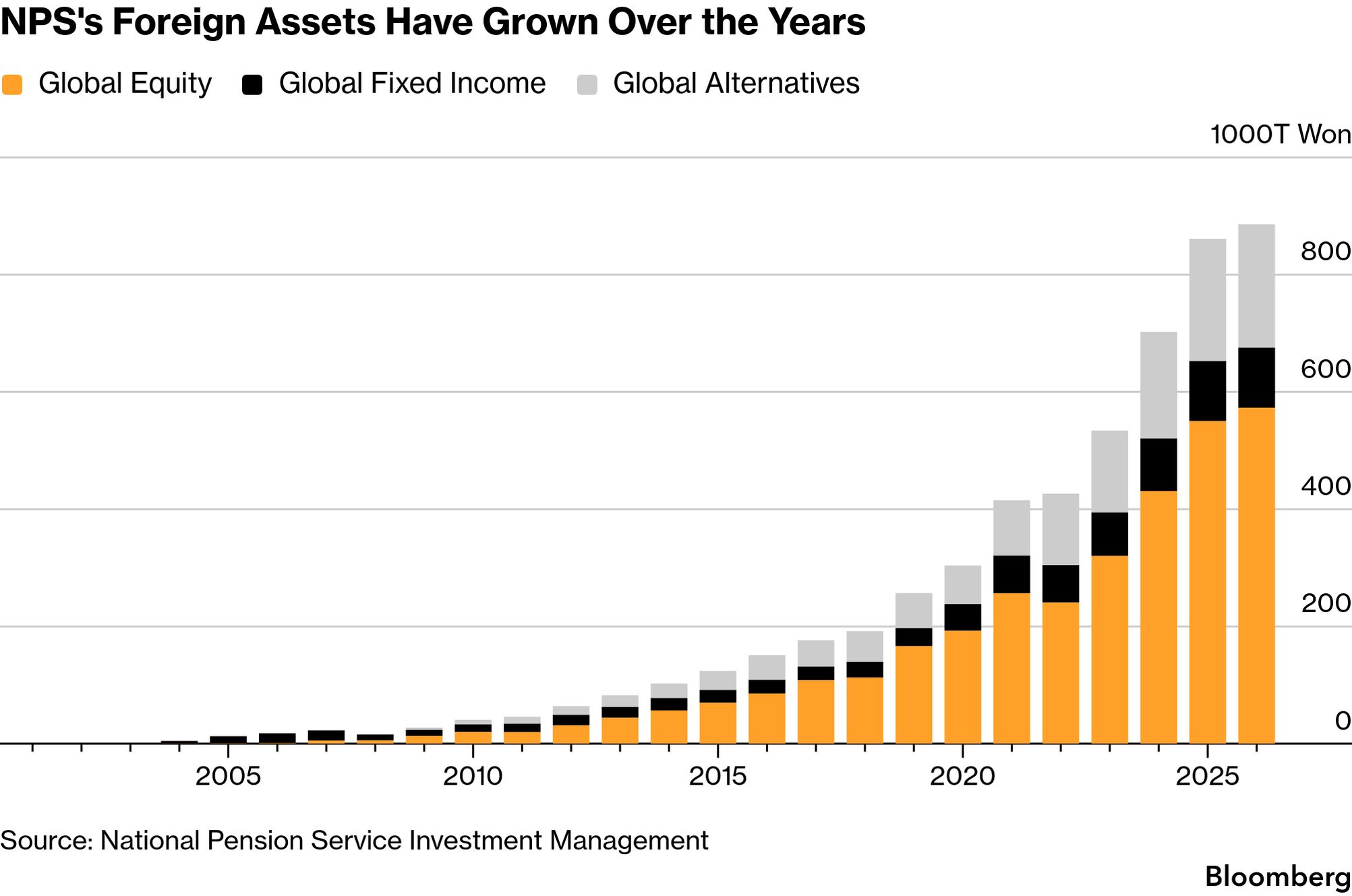

The fund has about in overseas assets, much of them in dollar-denominated investments. How the NPS manages its currency exposure has taken on greater significance after the won hit a 17-year low against the dollar on March 31.

Here are some key questions to consider about the change:

Why is NPS such an FX market heavyweight?

The NPS, as the world’s retirement fund, needs dollars for foreign investments and sells them when repatriating returns.

On a typical trading day, the fund is among the biggest currency traders in Seoul. Any shift in its hedging stance can move the dollar-won rate several figures within minutes.

What are its major FX hedging strategies?

The fund employs two main FX hedging strategies — tactical and strategic. Tactical hedging, traditionally capped at 5% of overseas assets, is used for short‑term, flexible moves to protect against sudden currency swings.

Strategic hedging is long‑term and planned, designed to manage currency risk over years regardless of short‑term volatility. Until the latest change, it had been capped for several years at 10% of overseas assets.

In April, the fund didn’t disclose how the new 15% baseline is split between the two strategies. While older meeting minutes detailed separate ratios, recent records omit the strategic figure, likely to prevent speculators from positioning around NPS’s activation moves.

When NPS hedges, it typically promises to sell dollars to major Korean banks later at a fixed price. To prepare, those banks immediately sell dollars in the local market. This increases the supply of dollars in Korea, which can strengthen the won. Neither NPS nor its counterparties disclose volumes in real time, and the banks never comment publicly on the trades.

The Bank of Korea doesn’t sit on NPS’s management committee; instead, its influence is exercised through its membership in a four‑party consultative body , established in November, that also includes the finance and health ministries and NPS.

Why is a pension fund involved in defending the won?

Simply put, the NPS, which is overseen by the Ministry of Health and Welfare, has grown too large to ignore.

Its foreign assets have already surpassed Korea’s official foreign-exchange reserves , which stood at $423.7 billion at end-March. In December, Bank of Korea’s governor at the time acknowledged that NPS, as a big investor, should consider its investment impact on the economy. That role will only grow as Korea’s population ages and pension outflows exceed contributions, forcing the fund to convert dollar‑denominated assets back into won to pay benefits.

By contrast, Japan’s pension funds, such as Government Pension Investment Fund , primarily invest on an unhedged basis, according to Bloomberg Intelligence.

Some market watchers remain wary of any heavy hedging practices by NPS. Hedging is costly, and using a pension fund to influence the currency risks creating political pressure to act when policymakers want the won to pivot to a certain direction.

In December, Korea’s finance minister said he has no intention of using NPS to defend the won, adding that recent hedging discussions were aimed at preparing for possible currency appreciation and ensuring stable portfolio management. In February, NPS Chairman and CEO Kim Sung-joo told a local news outlet it would be appropriate to return to a fully unhedged strategy once the country’s FX conditions stabilize.

How did NPS’s hedging strategies evolve?

NPS began in 2001 and has periodically adjusted how it hedges currency volatility.

A pivotal moment came in 2022, when the won fell sharply on Federal Reserve rate hikes. That year, NPS and the Bank of Korea reopened an FX swap line, and the fund’s management committee temporarily lifted its forex hedging cap to 10% of overseas assets. The program has been extended annually, culminating in April’s cap .

In April, NPS also adopted a currency‑neutral performance framework, allowing it to manage FX risk without those moves distorting official returns. It also laid out plans to issue foreign currency bonds in early 2027.

Its other tool — a currency swap line with the BOK — currently at $65 billion, expanded in size and duration each year since 2022.

What have been some of the more notable recent hedging activations?

NPS deployed tactical hedging in the weeks following former President Yoon Suk Yeol’s brief martial law declaration in December 2024, which sent the won sharply lower .

It tapped strategic in December 2025, after the won neared the psychologically important 1,500 per dollar level, by heavy retail outflows into overseas assets. In both cases, the currency quickly regained much of its losses before weakening again as underlying pressures persisted.