Collapsing Volatility Turbocharges Returns in Carry Trades

DoubleLine Capital and Van Eck Associates Corp. are among investors seeing renewed appeal in a currency strategy that’s revving up as the Middle East ceasefire helps steady markets and reignite risk appetite.

The carry trade — borrowing where interest rates are low and investing where they’re high — was already thriving as the war sparked a surge in oil prices that boosted commodity currencies such as Brazil’s real and Colombia’s peso.

But now it’s getting by the relative ebbing of international tensions, which has caused volatility in currencies, bonds and stocks to collapse. That backdrop is giving investors confidence that exchange rates won’t swing abruptly against them, as happened in 2024 when the trade combusted and roiled markets broadly.

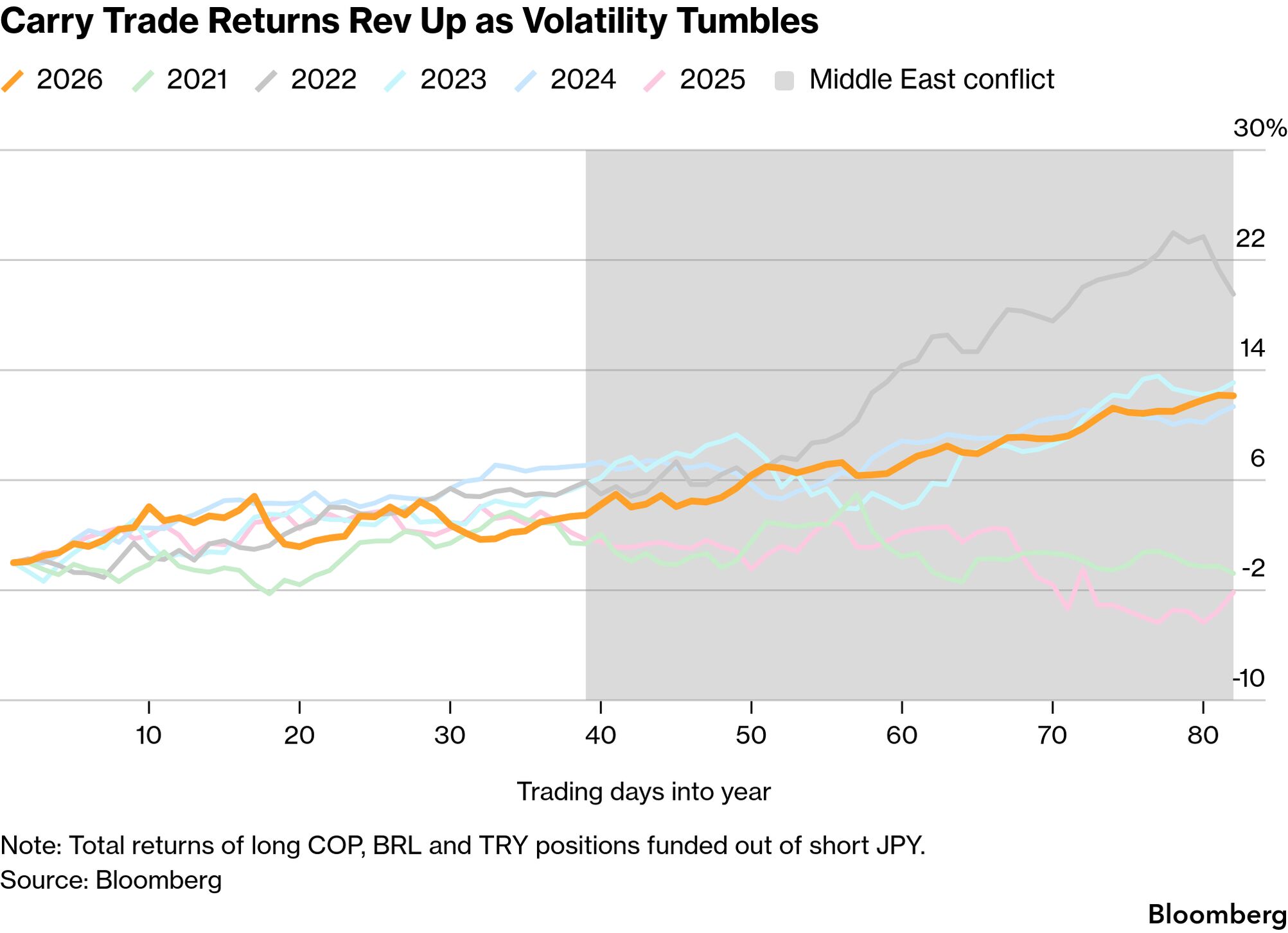

Banks including Citigroup Inc. and Goldman Sachs Group Inc., which have been recommending various iterations of the strategy for weeks, are sticking with the calls. One common version of the trade — borrowing in the yen to buy a basket comprising the Brazilian real, Colombian peso and Turkish lira — has gained about 12% in 2026, the best annual start in three years.

“Carry is back in control,” said Luis Estrada , a strategist at RBC Capital Markets. “Markets have recovered losses too quickly for most investors to participate, so they’re moving from hedging to a yield-seeking regime, while volatility is drifting lower.”

The waning market turbulence has energized trades across asset classes. In bonds, wagers that Treasuries will outperform interest-rate swaps — a bet that does well when volatility is low — got a lift from the ceasefire, while the S&P 500 Index set a record high this week.

Read more: JPMorgan Says UK Data Boosts Sterling’s Carry Trade Appeal

Optimism Abounds

“The perception of the war ending is the base case now, even if it may be overly optimistic,” said Anna Wu , a cross-asset strategist at Van Eck. “In particular, South American FX and yields are really strong at the moment thanks to their commodities links, which make them attractive for carry-trade bets.”

At RBC, Estrada suggests betting on Brazilian real gains versus the yen and Chile’s peso. Citigroup’s recommendations include Mexico’s peso, the real and the Turkish lira, while Goldman Sachs strategists have been telling clients to wager on an equally weighted basket of currencies — including the lira and Nigerian naira — against the dollar.

At Bank of America Corp., John Locascio , who heads Latin America currency-options trading, said hedge funds have been focusing on short-term trades looking for the Brazilian real to advance, while asset managers have been entering longer-term trades using digital options. These trades offer a fixed payout if the real reaches a specified higher level, effectively functioning as an all-or-nothing wager.

Locascio also said Colombia’s peso has gained “significant traction” in carry strategies in recent weeks despite the currency’s higher volatility and less-liquid status.

The peso is among the currencies that have benefited as costlier oil is expected to energy-producing economies at the expense of countries that depend on imported fuel. And while crude prices are down from their wartime peak, they’re still well above levels before the conflict erupted, keeping that dynamic intact.

“Emerging-market currencies of energy exporters outside the Middle East, particularly those currencies that have elevated real yields, can continue to outperform,” said Valerie Ho , a portfolio manager at DoubleLine. “Brazil’s real has emerged as a market favorite.”

Fragile Situation

Of course, the volatility backdrop can change in an instant given the fragile nature of the situation in the Middle East. US stocks fell on Thursday and oil rose as with peace talks stalled. On Friday, there were signs of of talks between Tehran and Washington.

For Jamie Patton at TCW Group, it all points to investors being too complacent.

“People are loading up the boats with risk in shallow water,” said Patton, TCW’s co-head of global rates. “However and wherever you look at risk being priced, it’s just too low.”

Another concern is that the popularity of the strategy only increases the peril for both traders and the economies they pour cash into.

Crowded wagers on emerging markets — and, on the other side, short bets against currencies like the yen — can spark a rush for the exits depending on global events or changing macroeconomic expectations. A prime example was , when a policy shift by the Bank of Japan helped upend carry trades, triggering a yen rally and jolting global markets.

Read more:

An International Monetary Fund report this month flagged the rising sensitivity of hedge-fund performance to emerging-market carry returns in recent years. That suggests the unwinding of these trades, typically considered the territory of hot money that can flee quickly in times of stress, could put pressure on developing nations.

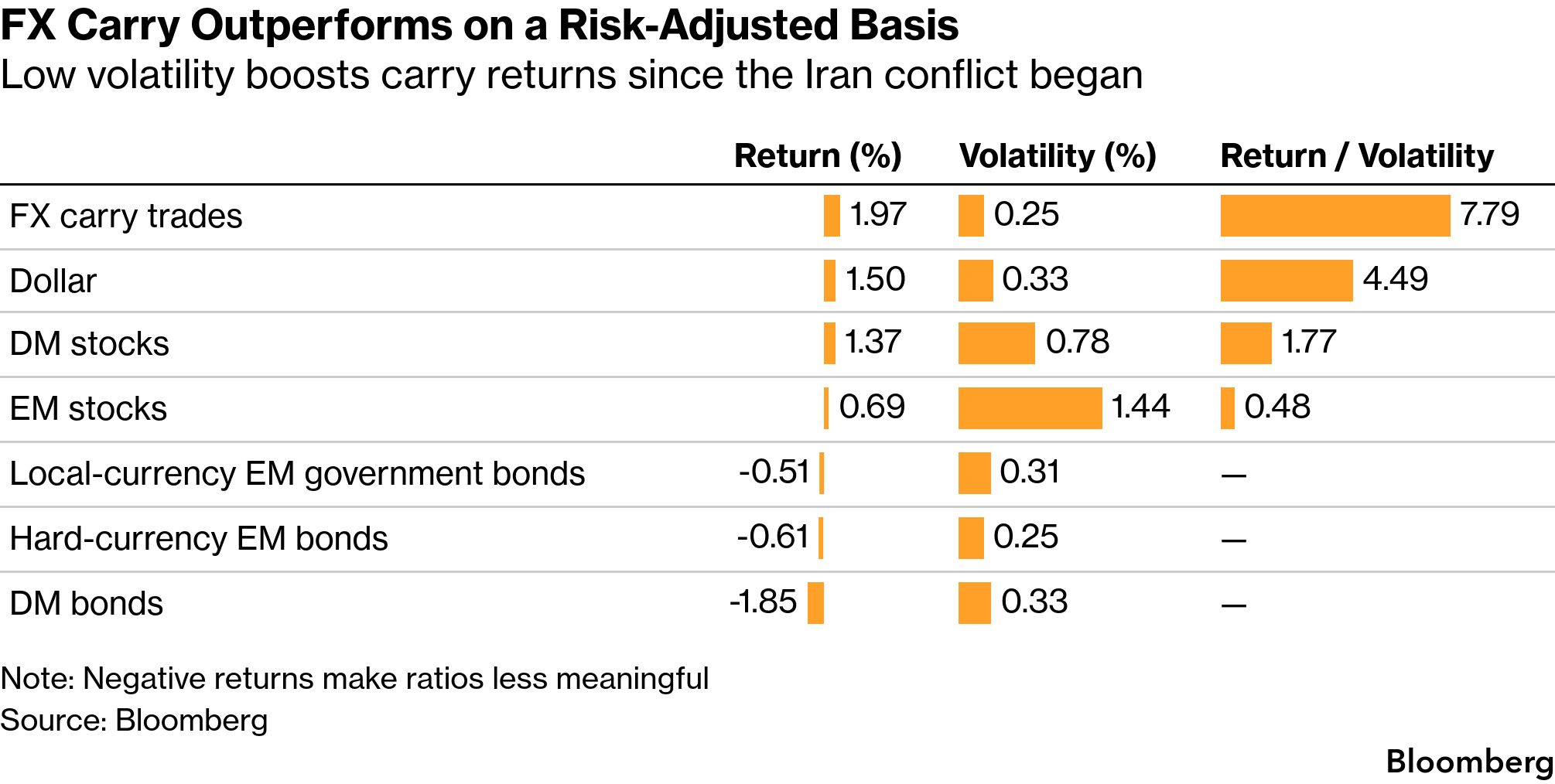

Risk Adjustment

For now, though, investors appear to be banking on the peace initiative to prevail. In currencies, a JPMorgan measure of volatility has tumbled from a multi-month high reached at the end of March, and is now around its lowest level since January.

That reversal is a boon for the carry trade because investors using the strategy rely on picking up small bits of yield over time, returns that can be swiftly wiped out by swings in exchange rates. So the calmer markets are, the better the approach looks on a risk-adjusted basis.

“Markets always look through to the other end, and the carry trade is an opportunity to make money in a risk-on environment,” said George Boubouras , head of research at hedge fund K2 Asset Management. “But we may see some reversals in the next 30 to 90 days, potentially because it’s run so well.”