Indian Rupee Set for More Chaos as Banks Unwind $30 Billion in Arbitrage Trades

The biggest shock to India’s currency market in years is set to worsen as banks prepare to unwind billions of dollars more in arbitrage trades.

The Reserve Bank of India’s to clamp down on bearish rupee positions late Friday sparked a race by bankers to plead for a rethink as they fielded anxious client calls and gamed out ways to limit losses on trades estimated to be worth at least .

When trading resumed on Monday, dealers encountered a panic-stricken market with thin liquidity. One of them compared the pressure of getting trades done to an intern performing open-heart surgery. While exact figures are hard to come by, people familiar with the matter estimate banks closed out anywhere from $4 billion to $10 billion of arbitrage positions targeted by authorities.

That means the vast majority of trades still need to be unwound before an April 10 deadline imposed by the central bank, unless authorities walk back their order. That possibility led some banks to stay on the sidelines Monday, even though the RBI has given no indication of backing down. Indian foreign-exchange markets are shut Tuesday and Wednesday for a holiday.

“Based on client data and NDF flows, it appears that around 25-30% of total positions could have been unwound on Monday,” said Ashhish Vaidya , head of treasury at DBS Bank in Mumbai. “That indicates fresh volatility in the currency market once trading resumes.”

The RBI’s move is one of its attempts in more than a decade to rein in currency speculation. After an initial jump, the rupee changed course and slid to a fresh low, highlighting the deeper pressures — from elevated oil prices to persistent capital outflows and a widening trade deficit. India is to the fallout from the Iran war and surging energy costs due to its reliance on imports. The currency closed around the 94.80 per dollar level on Monday, with the gap between the day’s high and low the widest since 2013.

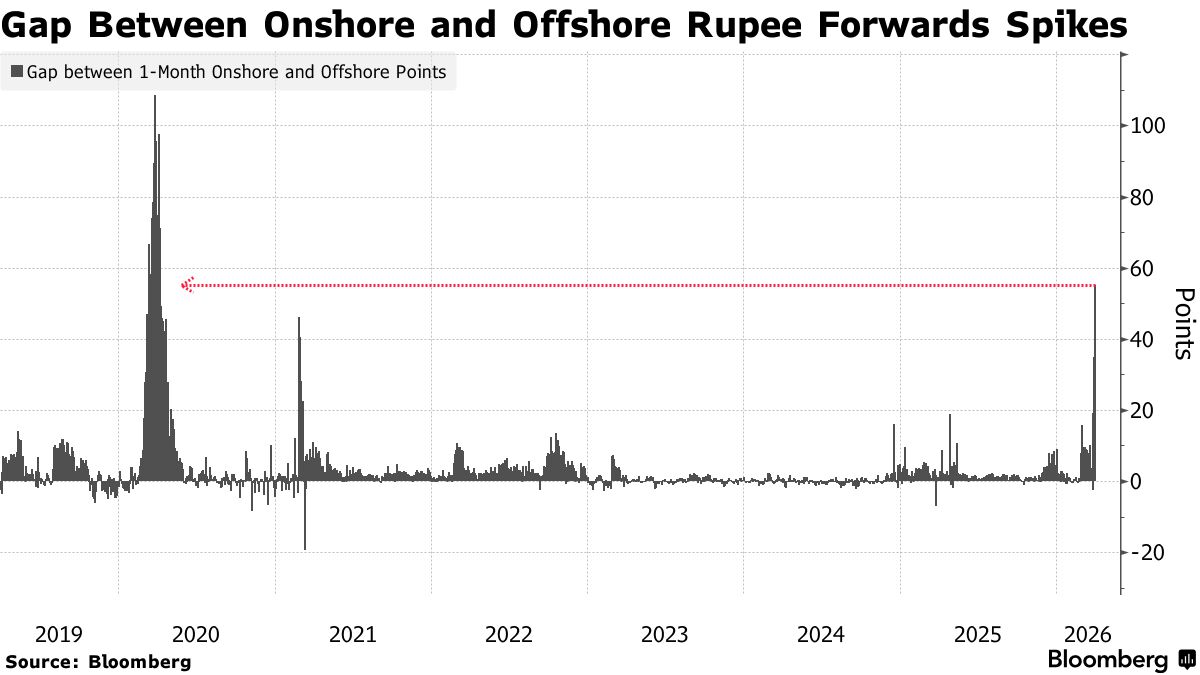

The directive left banks scrambling to unwind arbitrage trades, where they had been buying dollars locally and selling them offshore. As those positions were reversed, the gap between onshore and offshore forwards surged to the highest since 2020.

With only one trading session left this week on Thursday, volumes are expected to stay subdued at least for now. Banks have sought a delay to the deadline, but if the RBI offers no leeway by April 6, there will be sharper moves ahead. Requests for flexibility are still being made, the traders added.

Overnight implied volatility on the dollar-rupee climbed this week to the highest levels seen since November 2020, signaling traders are bracing for exaggerated price swings. The traders and bankers Bloomberg News spoke to have asked not to be identified as they aren’t authorized to speak publicly.

Exit Strategies

The early market moves followed a weekend of intense calls across treasury desks, as teams mapped out scenarios after the RBI’s announcement. Some were flooded with enquiries from offshore investors seeking clarity on how positions would be handled. At one foreign lender, staff fielded near-continuous calls through Saturday, with some spending more than half a day on the phone.

By Monday morning, many had already identified the need to reduce their exposures. Dealing rooms that would typically come alive closer to the market open were staffed before dawn, as banks rushed to assess exposures and prepare exit strategies.

One dealer said they began cutting risk as early as 8 a.m. in Mumbai, an hour before the official open, after spotting a sharp dislocation between offshore non-deliverable forwards and the domestic market. Within the first hour, a significant portion of positions had been reduced, the dealer said.

Still, most public sector banks held off from exiting positions at a loss on Monday, as doing so would have impacted their books on the last trading day of the financial year, according to another trader. That hesitation helped explain why the rupee gave up its early gains after the initial rally.

Several institutions chose to delay action in the hope that market conditions would stabilize or that some flexibility might emerge from the regulator. In some cases, banks explored alternatives, including whether positions could be transferred to other group entities.

India has imposed restrictions on currency positions before, such as in 2011, but market participants say the latest curbs hit much harder. The scale of FX operations has ballooned over the past decade. Earlier measures also tended to focus on aggregate positions, allowing banks to net off positions across onshore and offshore markets. The latest rules apply specifically to onshore, forcing a painful unwind.

The central bank’s move reflects broader concerns about the role of offshore markets in driving rupee weakness. Persistent demand for dollar hedges and speculative positioning pushed offshore forward points — the extra cost of locking in a future dollar–rupee rate — to elevated levels, leading to a cycle that encouraged further depreciation bets.

Authorities had previously tried to counter this through direct intervention, but at the cost of a in FX reserves.

Some strategists, including at Wells Fargo and VanEck, warn the rupee may weaken further to a record 100 per dollar or beyond if the Iran war drags on, despite authorities’ efforts to stem the decline. They cited elevated oil prices that will worsen inflation and the current-account deficit, with Monday’s price action highlighting the limits of the RBI’s measures.

Read more:

At a domestic private bank, a trader said the RBI’s move came as a surprise, unlike past actions that were typically preceded by verbal warnings or steps to curb offshore participation. Although the bank didn’t unwind much on Monday, it took a mark-to-market hit as the spread between onshore and offshore markets widened on the last trading day of the financial year, the trader said.

With fears of further RBI measures, the bank now plans to gradually unwind its positions in the coming days, the trader added.

Barclays Plc analysts said Monday that while the initial impact of the RBI’s cap may fade, further measures to defend the rupee are possible, including even tighter limits on banks’ positions, greater restrictions in the NDF market, and steps to manage dollar demand or encourage capital inflows.