Iran War Spurs Emerging Markets Rout, Threatens Investment Case

The war in Iran has swiftly turned emerging markets into one of the worst places to be for global investors.

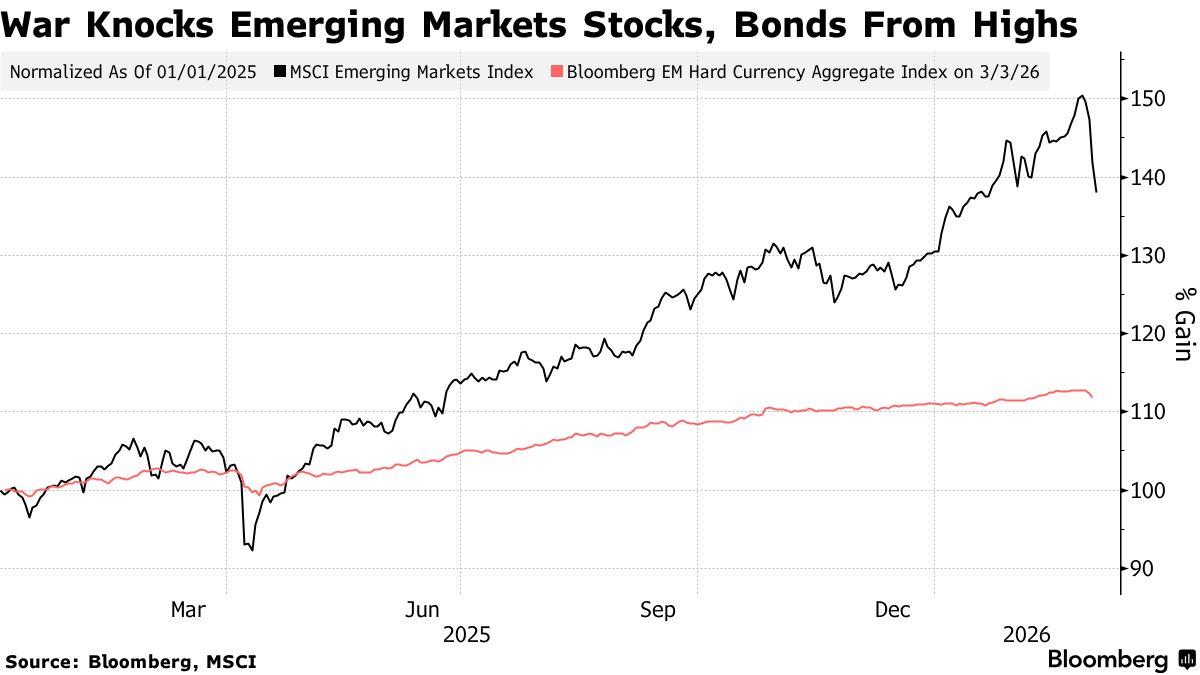

Stocks and bonds that only days ago were at record highs are now under pressure as traders assess how higher oil prices and a resurgent dollar — twin shocks unleashed by the conflict — weaken the outlook for some of the world’s fastest-growing economies. Asia has borne the brunt of the selloff, with Korean stocks 18% this week.

The abrupt shift is raising concerns about whether the investment case for emerging markets has changed. Before the war, top money managers had been across Asia, Latin America and parts of EMEA, betting on robust growth, easing inflation and looser global monetary policy. Now, the prospect of persistently higher energy costs and a stronger dollar risk triggering a rush to cut exposure.

“The resilience of emerging markets will now be tested, and here we might see the strongest impact after a very strong start to the year,” said Sonal Desai , chief investment officer for fixed income for Franklin Templeton.

The slump in EM stocks deepened on Wednesday, with the benchmark index falling as much as 4.4% and edging closer to a technical correction. By comparison, MSCI Inc.’s gauges for global and developed-market equities were down less than 1% ahead of the US market open.

A of dollar-based EM debt has posted its biggest two-day slide since April, while a measure of currencies has dropped 1.7% since Monday, heading for its steepest weekly decline since March 2020.

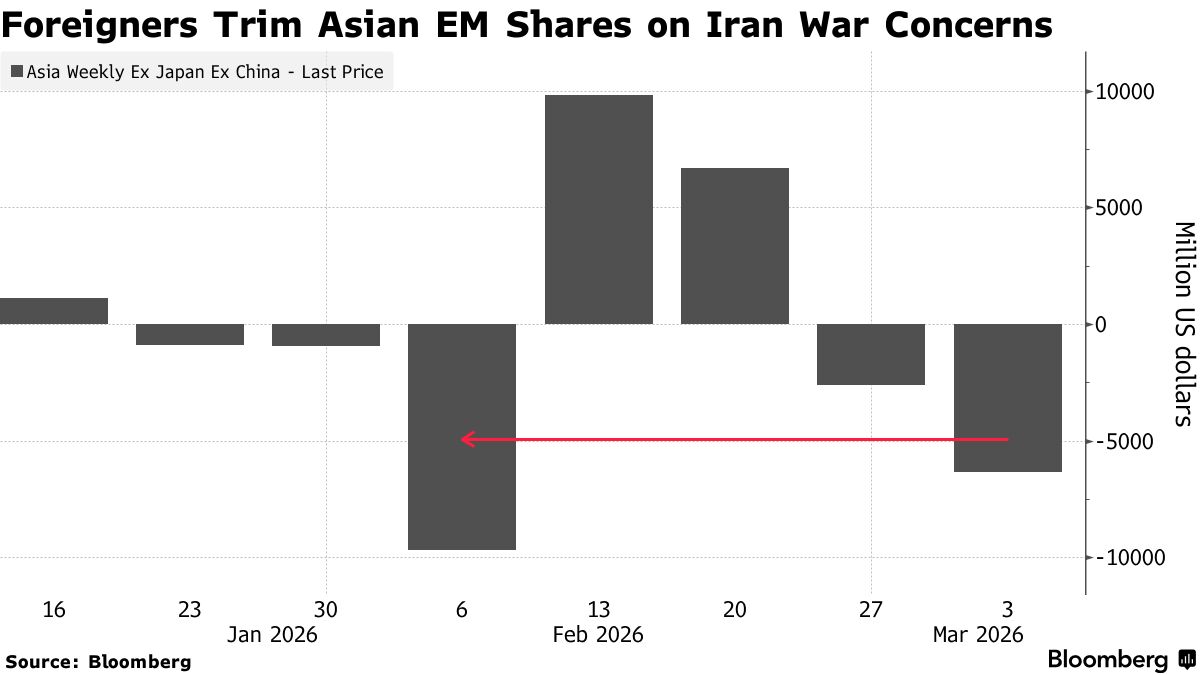

Fund flows reflect the souring mood. Global investors pulled $6.3 billion from Asian EM stock markets excluding China this week, putting the region on track for its largest weekly outflow in a month, according to data compiled by Bloomberg. Chipmaker-heavy markets such as South Korea and Taiwan — among the main beneficiaries of this year’s rally — led the retreat.

Read more:

For many investors, the immediate question is how to reposition portfolios for a world of higher energy prices. A key strategy emerging across desks is to differentiate between winners and losers based on exposure to oil, selling large importers and rotating into exporters.

“While we believe it is too early to add risk outright, we have already been rotating away from oil‑sensitive importing countries toward oil exporters in more neutral geographies as energy prices rise,” said Marcelo Assalin , head of emerging markets debt at William Blair, adding the firm is underweight the Middle East.

Across Asia, importers such as South Korea, Thailand and India are vulnerable to sustained oil price increases, while exporters like Malaysia may be more resilient. Higher crude costs threaten to push up consumer prices, the outlook for some central banks that had only recently begun to contemplate rate cuts.

Read more:

In Latin America, the impact appears mixed . Higher oil benefits exporters such as Colombia and Mexico, though any fiscal windfall could be offset by fuel subsidies, Bloomberg economist Felipe Hernandez said. At the same time, both countries face the greatest inflation risks that could keep rates elevated.

A stronger dollar adds to the strain, with the Bloomberg dollar gauge up 1.5% this week. That’s pressuring currencies across the developing world and raising debt-servicing costs. Large energy importers “such as Thailand, India and Northeast Asia are obviously the most vulnerable from an FX standpoint,” said Philip McNicholas , Asia sovereign strategist at Robeco Group in Singapore.

India’s rupee fell to a record low on Wednesday, prompting the central bank to sell dollars to support the currency, according to traders. It joins authorities in countries such as Indonesia and Turkey that have to stem losses. In China, the central bank set a just days after signaling tolerance for weakness, abruptly switching course.

Bonds Outlook

The outlook for bonds is more nuanced. If economic growth remains soft, long-term interest rates may have room to fall. That would flatten yield curves in markets where longer-dated yields look elevated, potentially creating value in those maturities.

“The longer-end of the curve should grind lower overall given subdued nominal GDP growth indicating that curves such as Thailand and Korea are too steep,” McNicholas said.

Whether the pullback in EM proves temporary or signals a deeper shift depends on how the war evolves. President Donald Trump on Tuesday the US would provide insurance guarantees and naval escorts for oil tankers and other vessels through the Strait of Hormuz, aiming to head off a potential energy crisis caused by the conflict.

For Asian equities, Goldman Sachs Group Inc. said spikes in geopolitical risk typically have a negative short-term effect but dissipate over time. The war comes as parts of the region were already vulnerable to a correction.

“Strategically, we remain positive and view short-term weakness as an opportunity to build positions in key themes including defense, power, and shareholder return,” Goldman analysts led by Timothy Moe wrote in a note.