Upside-Down Market Has EM Currencies Calmer Than Developed Peers

Emerging markets are supposed to be far more volatile than developed ones. But in currencies, that’s been turned upside down this year.

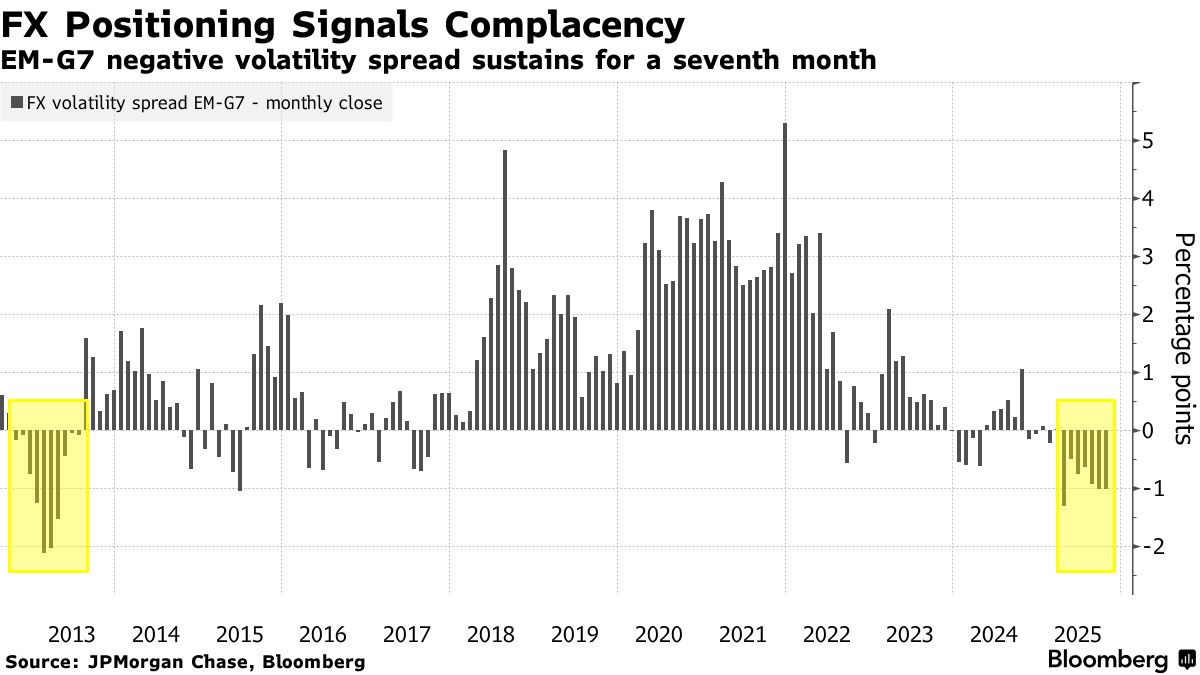

An index that gauges the expected swings for developing-nation currencies like the South African rand and Brazilian real has stayed below the same measure for developed nations for seven months, according to JPMorgan Chase & Co. indexes.

It’s unusual for that gap to persist for so long and some money managers say it suggests a lack of concern about riskier markets. While investors like Ninety One’s Christine Reed don’t see a slump as a given, the inversion appeared in the year before the 2008 collapse, ahead of the euro-zone debt crisis and before the so-called taper tantrum 12 years ago amid fears the Federal Reserve would slow its stimulus.

“There is perhaps a degree of complacency,” said Reed, an EM fixed-income portfolio manager. “Inversion does not mean a crisis is imminent, but it is a theme to keep a close eye on.”

Bets on lower US interest rates, signs of a faltering economy, and renewed trade-war concerns have contributed to a falling — and prompted investors to bet on developing nations.

The opportunity to reap higher returns in emerging markets has driven the biggest rally since 2017 for their currencies. And the inflows are keeping volatility below their developed-market peers, according to Brendan McKenna , EM economist and FX strategist at Wells Fargo Securities in New York.

“Emerging markets have more-attractive real rates and many have a degree of political stability associated with them, at least for now,” McKenna said. An uptick this year in political uncertainty in the euro region, the UK and Japan, has “induced more volatility,” he said.

A look at the JPMorgan index shows the discrepancy: At-the-money forward volatility on three-month options for emerging-market currencies stands at 6.75%. That’s seen annualized swings fall by 240 basis points this year. The same measure for developed-market currencies has seen a smaller decline of 181 basis points and is currently at 7.41%.

In April this year, when US President Donald Trump’s shock trade tariffs sparked a retreat from the dollar, EM currencies had an implied volatility that was 1.4 percentage points lower than swings in rich nations — the widest spread in nine years.

While the inversion itself isn’t unusual, it rarely stays that way for multiple months. On the occasions when it does, markets have suffered, Ninety One’s Reed says.

“We’ve seen this pattern before,” Reed said.

While Argentina and Turkey stand out as recent exceptions, emerging markets are a lot more resilient than they were during past market downturns. They have bigger currency reserves, more balanced trade and investment flows and are much less reactive to global shocks, Reed said.

That’s helped “decouple an inversion from an immediate crisis signal,” she said.